The US-Israel war on Iran revives inflation fears

Kudos to the Statistical Center of Iran for not missing last month’s inflation report (Khordad = 21 May-20 June), despite the destruction caused by the Israeli bombing of Tehran. The attack struck at the heart of Tehran, a few blocks from SCI’s main building. Significantly, for those who habitually question Iran’s official statistics, the report is not flattering.

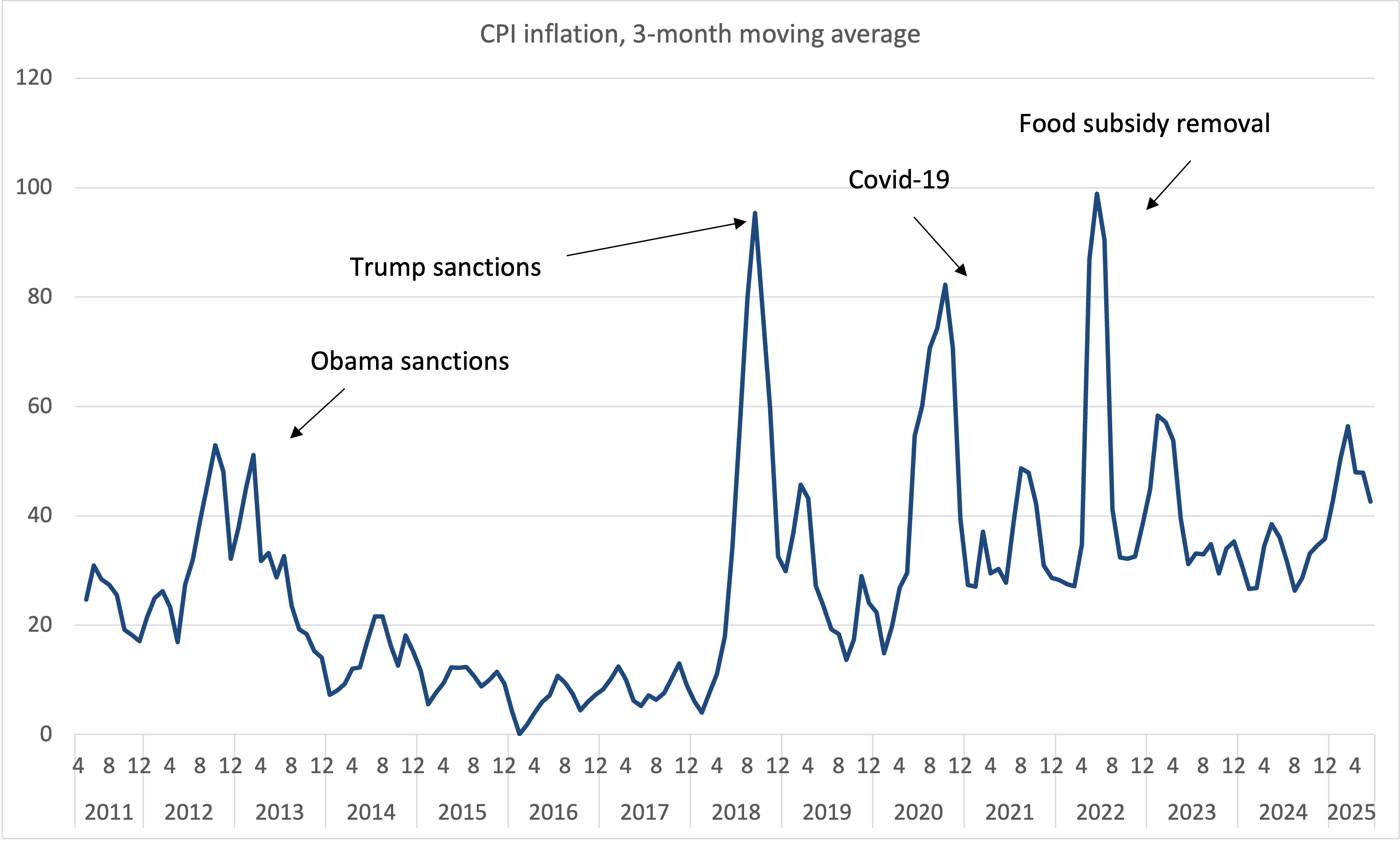

I have incorporated the new data in my moving-average graph (Fig. 1), which has appeared before in these pages. The drop in the past few months hides the fact that prices jumped by 3.3% in khordad (an annual rate of 48%) compared to 2.7% the month before. Inflation, it seems, is back to its high level two months ago when the CPI jumped by 3.9% (58% annual rate!).

The temporary slowdown in May was closely linked to a 20% depreciation of the rial against the US dollar. This depreciation reflected Iranian optimism about the potential outcome of the latest negotiations with the Trump administration aimed at preventing war that had begun last April. Unfortunately, that optimism overestimated the power of international laws and norms of diplomatic engagement in restraining Israel and the United States: Israel started a war with Iran on June 13, two days before U.S. officials were scheduled to meet their Iranian counterparts for a crucial, last-ditch effort to avoid conflict. The US, which had backed Israel’s leap into the unknown, joined the fray ten days later by bombing Iran’s nuclear sites, all under IAEA inspection.

The invasion altered more than just Iranian perceptions of the so-called rules-based international order — it caused a 25% devaluation of the rial, pushing the free-market exchange rate back to its previous peak. This depreciation will show up in higher local prices in the next month or two, though at this moment, living under the threat of Israeli warplanes have overtaken inflation as the primary concern for most Iranians.

Had Israel not invaded Iran when it did, the exchange rate would likely have remained around 800,000 rials per USD, allowing inflation to fall below 30%. It is not too far-fetched to assume this; Israel has long been wary of any return to normalcy in Iran, as that would reduce the effectiveness of its deterrent strategy. In that light, the timing of the invasion appears to have been a calculated decision.

The depreciation of the rial is only one factor driving high inflation. Another major contributor is the budget deficit, which is largely being financed through money creation. I do not have precise data on how much of the deficit is funded by newly printed money. In particular, I am unsure how the recent increase in cash transfers has been financed.

In March, Iran’s Ministry of Cooperatives, Labor, and Welfare (MCLW) added 5 million rials’ worth of food coupons to the monthly cash transfers received by individuals in the bottom four income deciles, and 3.5 million rials for those in the next three deciles. When cash transfers were first introduced in 2010, they were funded by higher energy prices charged by the government. The source of funding for the recent increase appears to be general revenues—which are already insufficient to cover existing expenditures. (Why the government chose to incur the added distribution costs of subsidized food, rather than simply increasing cash payments, is a question for another time.)

Whatever criticism one might raise against the coupon program, its timing was impeccable. It provided some much-needed relief to low-income households just as U.S.-Israeli actions once again disrupted ordinary life in Iran.

leave a comment