Is the Tehran Stock Exchange a good barometer of Iran’s economy?

The Tehran Stock Exchange (TSE) has been in the news lately, not because its 22-month downward slide has ended but because four cabinet members highlighted its plight in a letter to President Rouhani. The letter was written on September 9 but came to light last week. The brouhaha that followed, however, was not about the TSE and what its poor performance means for the economy, which appears to be heading for a double-dip recession. Attention has instead focused on division within Rouhani’s coalition government and what it means for the future of his austerity program. I wrote about these issues for Al Monitor last week; here I’d like to take a closer look at the performance of the TSE — how badly it has done, and why.But before getting to the numbers, it is worth repeating here something I noted in my Al Monitor piece, that the TSE is not big enough or transparent enough to have the level of influence of the big stock markets in advanced economies. In Iran the TSE’s economic influence is limited by too much influence by government-owned banks and enterprises, and a lack of a legal infrastructure that protects ordinary investors against insider trading.

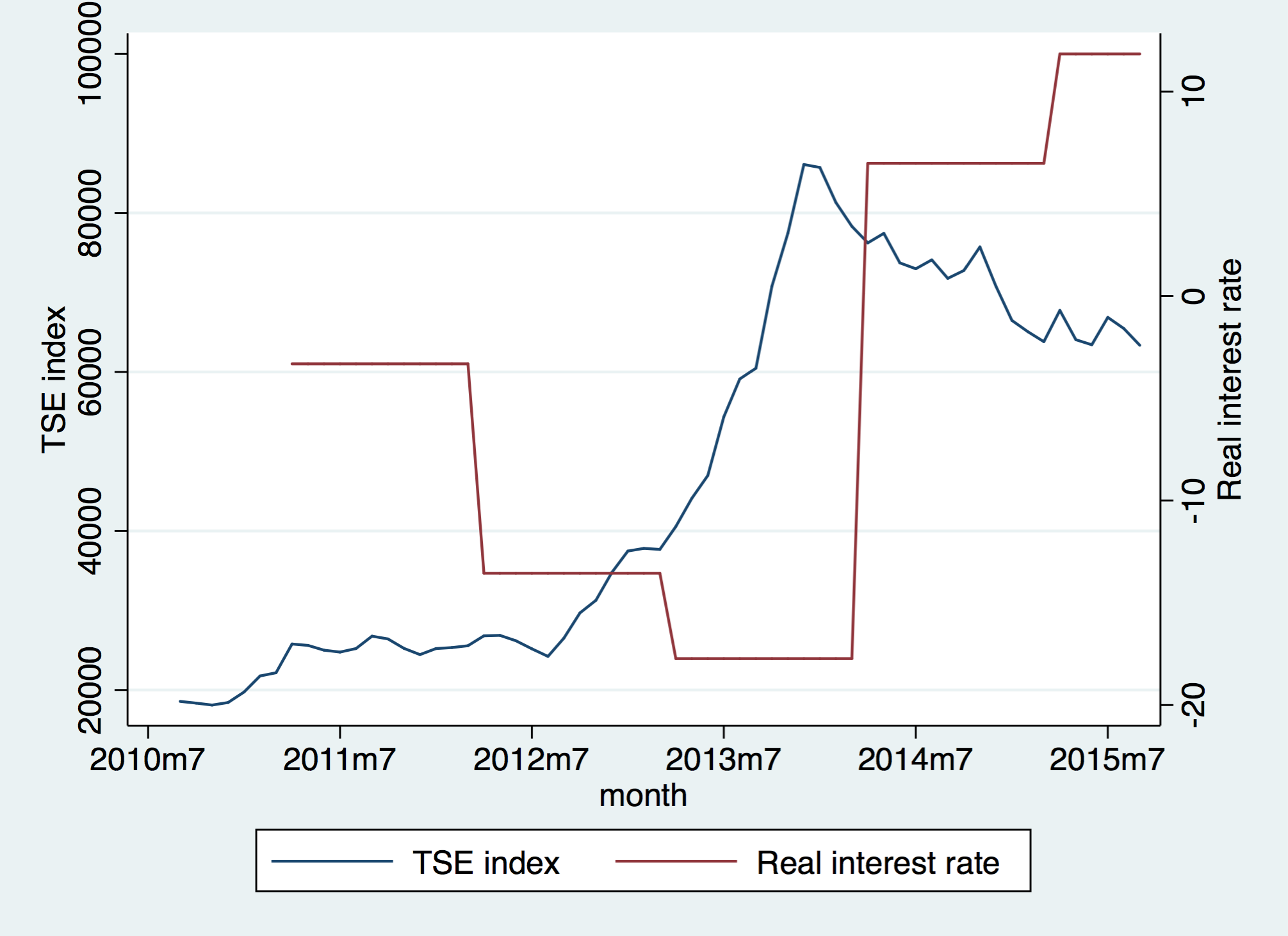

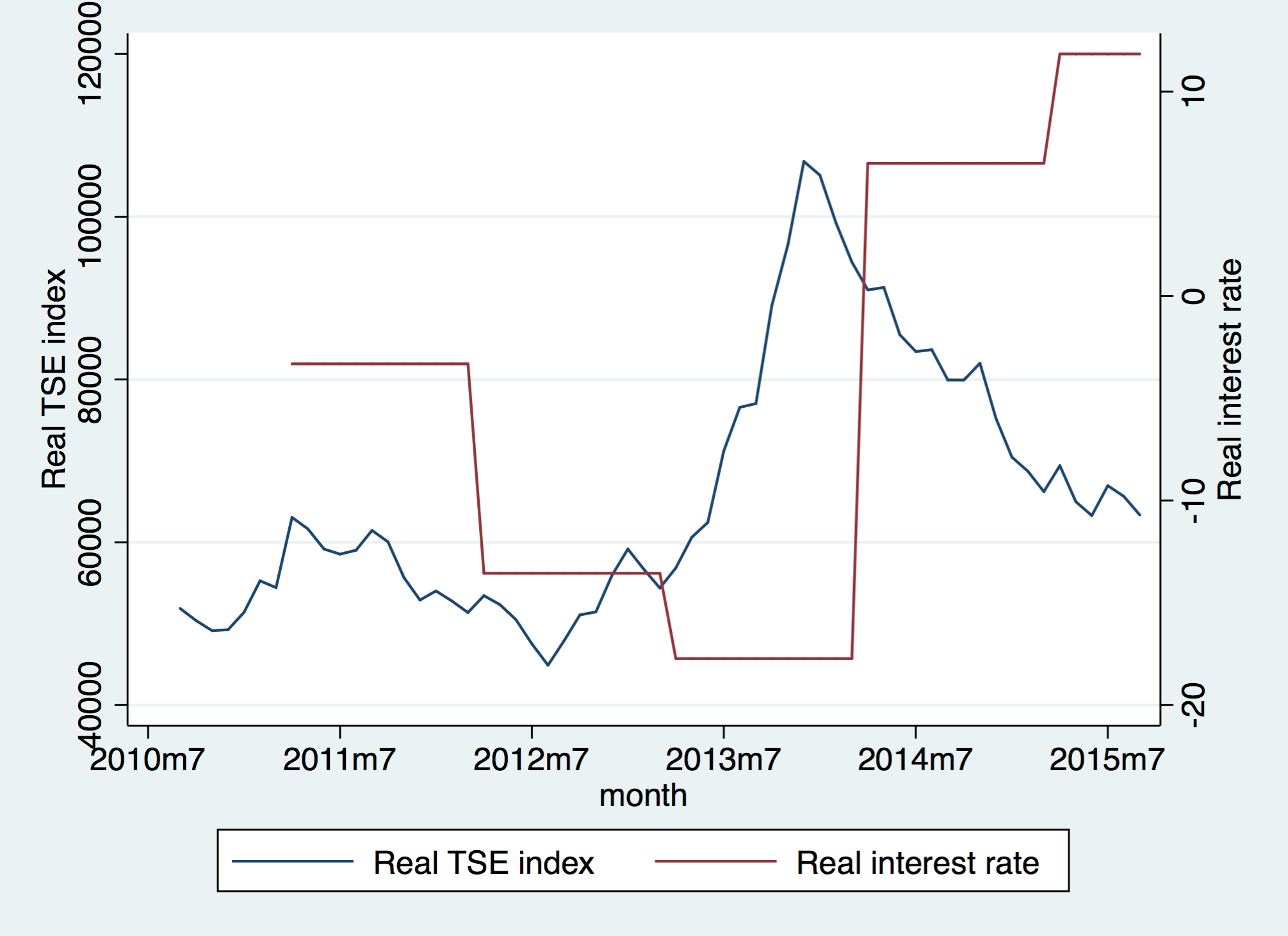

As for performance, the TSE index has taken a serious beating since December 2013. It reached close to 89,000 points (see graph of nominal values on the left) before falling to less than 65,000 in early September, when the ministers’ letter was written. This is a loss of more than one-third in the value of the index, and a similar loss in the wealth held by those who hold its stocks. The decline in the index is even sharper when you correct for inflation (right graph), registering a loss of 48%.

Figure. The TSE index (average monthly nominal values on the left graph, real values on the right) and the real interest rate.

Notes. Monthly averages of the TSE index are calculated from daily values, and the real values are obtained using the Central Bank of Iran Consumer Price Index.

Source: The TSE index was downloaded from the TSE website; interest rates on one-year deposits and the CPI are from the Central Bank of Iran.

But, before you feel too sorry for TSE investors consider the amazing run they had up to December 2013. In the two years before heading south, the index had risen by 252% in nominal terms and 100% after accounting for inflation. Even with the sharp decline since 2013, between December 2011 and September 2015 the index gained 9.4% per year in real terms. Not bad for an economy in recession and with negative interest rates.

If I had added the growth rate of the GDP to this graph it would have been obvious that the TSE is not a good barometer of Iran’s economy. It rose when the economy was doing badly — during 2012-13 — and fell when it actually started doing better.

If the TSE does not reflect the health of Iran’s economy, what does it reflect? What explains its violent up and down in recent years?

I have to confess that explaining the behavior of stocks is not remotely in my fields of expertise, but the graphs above offer a rather standard explanation that is worth thinking about. Stocks were increasing in value when interest rates were negative in 2012-2013 (perhaps because people were fleeing banks), and falling when interest rates rose sharply in mid 2014.

Real interest rates (nominal one-year deposit rates minus the rate of inflation) were negative until 2014, falling below minus 17% in 2013-2014, when inflation reached 35% and nominal interest rates were capped at 17% per year. After Rouhani’s election, and thanks to his austerity program, inflation fell to 15% per year while interest rates rose to 22%. Real rates thus turned sharply positive, first to over 6%, where they stand now.

High interest rates can negatively affect stock prices because they attract money away from stocks and into lucrative bank deposits. This is hardly surprising at a time when company values are in doubt because industrial production has slowed down (actually fell by 2% during spring 2015, as reported by the Statistical Center of Iran), the oil market is very weak, and the fruits of the July nuclear deal are yet to come.

There is no doubt that the high price of credit is an important reason for the weak recovery, or what the IMF suspects is a double-dip recession. Tight monetary policy has no doubt played a role in keeping interest rates high and contributing to the stock market’s blues. But knowing this is not the same as knowing how to bring interest rates down or raise the TSE index. High interest rates are the result of a deep banking crisis that started several years ago under Ahmadinejad, and made much worse by the fall in the price of oil. The banking crisis cannot be solved and interest rates brought down by printing money.

On a final note, I find it curious that in their letter to President Rouhani, the four esteemed ministers — the portfolio of three of whom concerns the economy — chose to focus on the weak TSE index instead of something more relevant, like unemployment. Focusing on the TSE has made them seem overly concerned with the fortunes of the rich, who own equity, and little with the suffering of the unemployed, the poor, and even the middle class, few of whom own stocks. It is particularly unseemly for a labor minster — one of the four signatories — who likes to think of himself as the champion of the working men and women. They would have all been much better off focusing on high interest rates, the credit crunch, and the lack of progress in employment.

{kind=link}

[…] rial barely moved as “implementation day” arrived. The Tehran Stock Exchange, which has been depressed for the last two years, did gain about 4% during the week before. But compared to the weight of the sanctions being […]

Dear Professor Salehi,

Does it not matter that most companies quoted on TSE, by only amortizing their assets at the dollar/Rial rate of the time of investment, today own outmoded and inefficient machinery and no reserves to renovate those assets? If energy subsidies be removed these companies will fall like a house of cards.