Inflation and money supply in Iran: a closer look

Last week, in a post on the Lobelog.com I noted further signs of moderating inflation. Prices in the Iranian month of Dey (ending 20 January 2013) rose by 1.7%, compared to 2.5% the month before and 4.5% per month in the previous two months after devaluation. These are high rates of inflation on an annual basis (see chart below), but a sign that the Central Bank may have found a way to keep the growth of money supply below the rate of inflation. I was curious enough if this were the case to look up money supply data published by the Central Bank and here is what I found. For the quarter that ended on December 20, 2012, which covers the three month period after devaluation, the rate of growth of money supply was 20 percentage points below the rate of inflation.

The reason why this is noteworthy is because it indicates that large devaluations are not necessarily followed by runaway inflation. In a non-oil exporting country, it would have been very difficult for the government to keep money supply growth this far below inflation if its currency were to lose half of its value. But thanks to oil income, the Iranian government did not have to print money as fast as the currency was losing value after last October’s devaluation. It chose instead to sell a significant part of its currency at lower rates, which is to say that it decided not to monetize its foreign exchange reserves at the free market exchange rate. Thus oil income helped keep the growth of money supply from exploding. It was missing this point that led to the widespread speculation about hyperinflation.

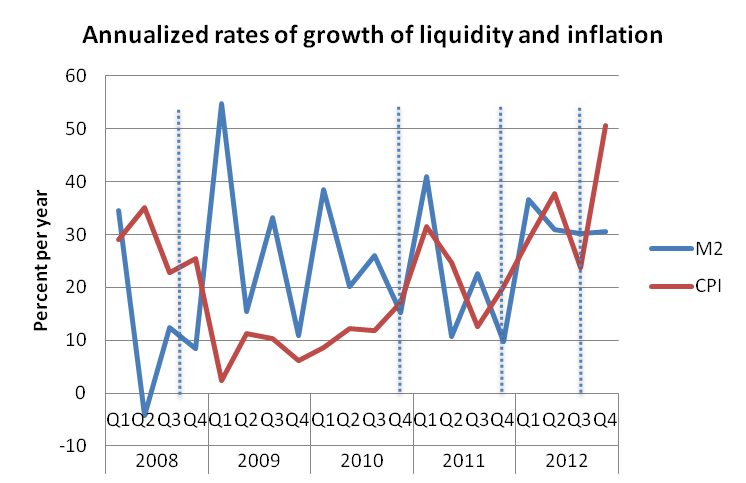

The charts below show how erratic the growth rates of money supply and CPI have been in recent years. The annualized inflation rates in Figure 1 show clearly the impact of three separate events on inflation (marked by vertical lines) — subsidy reform in December 2010, US financial sanctions in December 2011, and the collapse of the rial in October 2012. Each time prices spike but then they resume their normal pace of growth.

Putting inflation and growth of liquidity together in the second chart you notice that money supply, too, spiked after the first two events (2010Q4 and 2011Q4) but it did not after the devaluation shock. This time, the Central Bank seems to have put more emphasis controlling inflation. It chose to keep the growth of money supply steady, though not contracting, at about 32% per year. Those who blame inflation in 2013 on subsidy reform two years earlier should take a close look at how money supply and prices have behaved after 2010. The impact of subsidy reform on prices had largely dissipated by the end of 2010 when sanctions struck.

Figure 1. Annualized rates of inflation based on monthly CPI data (Source: The Central Bank of Iran).

Figure 2. Liquidity and inflation based on quarterly data (Source: The Central Bank of Iran).

If you want to trace inflation further back to 2008, when the Great Recession in the industrialized world began and oil prices fell to $40 per barrel, follow the charts in Figure 2. The chart to the left in this figure shows the annual rates of growth of liquidity (M2) and the CPI (inflation), and the one to the right shows the levels of these variables. The first burst in money supply came in the last quarter of 2008, when the Great Recession hit Iran in the form of lost oil revenue, to which the government reacted by expanding money supply. At this time, inflation was still below 10% per year, and would take a full two years of expansion well ahead of inflation before the subsidy reform would push prices up.

This chart marks the four critical events since 2008 (oil price collapse, subsidy reform, US financial sanctions, and devaluation) and shows that after each event, money supply increased, except for the last one. It shows clearly that the high inflation that afflicted the economy in 2011-12 had its origins in earlier years. The mounting pressures on prices accumulating since late 2008 were suppressed by large inflows of foreign exchange that kept the rial highly overvalued. This is what I have elsewhere referred to as suppressed inflation, which devaluation unleashed. (Incidentally, if you want to see how silly some of the recent discussions about Iran’s economy have been, compare the money supply depicted in these charts with this strange graph of Iran’s money supply).

How long Iran’s monetary authorities will be able to hold the line on money supply is anybody’s guess. With mounting challenges to Ahmadinejad power, the Central Bank may be able to act independently enough to prevent more government spending from further destabilizing the economy. But, with serious talk this week of giving every Iranian 200,000 toomans (about $130 PPP) this March as a Nowruz gift, and inflation seemingly under control, chances are good that the parliament would authorize Mr. Ahmadinejad’s last populist injection of money into the economy.

با عرض سلام.لطفا” وبلاگی هم به زبان پارسی پیرامون شرایط اقتصادی کشور منتشر کنید تا ما دانش آموزان دبیرستانی که اونقدر انگلیسی بارمون نیست از تحلیل های روشنگرانه و زیبای شما استفاده کنیم.

سپاس گزارم.

Thank you for your interest. I am sorry, I am very slow at typing in Persian. But I appreciate your interest.

This posting makes a valid point that so far there is no sign of hyperinflation in Iran and that the high rates of inflation experienced in Iran during September through November of 2012 may have subsided somewhat in December and January. At least this is what the recent data released by the Central Bank of Iran suggests. However, the claims that the rate of inflation has continued to fall in January and is likely to remain under control are not warranted based on the available data. Djavad argues that during the last quarter of 2012, the Central Bank has kept money supply growth steady and below the rate of inflation. He then concludes that the rate of inflation is continuing to decline because of this policy. In my view, these arguments and the evidence presented in the pasting are not convincing. Here are the reasons why I find the argument problematic:

1. The data presented in the figures are not seasonally adjusted. If one adjusts the inflation series for seasonal effects (using monthly data since 1990), it soon becomes clear that between the months of Azar and Dey (roughly December-January), the rate has remained practically unchanged at an annualized rate of about 30 percent. The reason is that inflation tends to decline somewhat in the months of Dey.

2. Applying seasonal adjustment to the quarterly series for money supply since 1990 further shows that the money supply tends to drop in the fall season by an average of about 10 percent. As a result, the steady growth observed in the unadjusted series in Figure 2 actually means an acceleration relative to previous years.

3. Because of high inflation and economic instability, there seems to be increased currency substitution in Iran these days. In other words, people are reducing their holdings of rials and increasingly using gold, foreign currency, and other instruments as short term store of value. As a result, inflation may grow wild even if the money supply growth is kept under control. Indeed, unlike more stable countries where M2 grows faster than inflation, in Iran it has been growing by about 3 percent slower than inflation.

4. Finally, it is important to keep in mind that in the short and medium runs, money demand is rather unstable and the relationship between money supply and inflation is at best tenuous. So, it is not easy to attribute the pattern of inflation to the trends in money supply on quarterly or even yearly basis. Notice, for example, that the Fed has increased money supply very rapidly in the past five years, yet there is no sign of high inflation in the US economy. In Iran, inflation was rising between 2006Q3 and 2008Q3, while money supply growth rates continually declined and eventually reached zero for one quarter before the rate of inflation responded.

The bottom-line is that if people don’t trust the country’s policy-making process, inflation may rise even if money supply growth slows down. That kind of trust does not seem to have be reestablished in Iran. So, we may well see inflation flare up again in the next few months.

Greetings Dr. Salehi-Isfahani,

My name is Enrique Maduro, and I’m working with Orlando Monagas on our Degree Research Paper on Iran’s Subsidy Reform’s impacts. We are form the Universidad Metropolitana in Venezuela, and we have read your work about the impact of the reform on households and almost every single one of your blog posts on the subject. They have been very helpful in sight that, as you mention, there is almost no official information about Iran’s economy in the recent years. The information we have gathered from your publications have been very valuable for our work, and is because of that that we would much appreciate if you accept us to interview you via email, skype, phone or facetime.

Thank you for your time.

Best Regards,

Enrique Maduro & Orlando Monagas

enriquemaduro91@gmail.com

I am hopeful his 200K payment plan will not be approved by the parliament as from the perspective of his political foes it will look like pre-election vote-buying.

By the way, I think “hyperinflation” folks are technically right to some extent, however what they are analyzing is not what we need to analyze here. Yes, from the perspective upper middle class families the inflation has been very high, however that is not true from the perspective of most of Iranians or the majority of Iranian economy. The economy is obviously under pressure but it is far from being in critical failure state. It would be interesting to compare signs of complete economic melt-down observed in other countries with Iran. Were they in the same state after similar amount of time passed devaluation?

PS: there was a tendency among liberals to argue that sanctions work so there is no need for a war. However the reality will eventually kick in, either US will moderate its demands regarding Iran’s nuclear program and will reach a compromise with Islamic Republic or will drawn into a military conflict. With Obama in second term and no stomach for another war in middle east the more likely options seems to be an agreement similar to the one Regean reached with China or the continuation of the same containment and pressure policies for another 4 years and leaving the issue for the next president.

Considering the hard-line non-compromising republican position and Israel friendly democrats a grand bargain can only happen only through secret negotiations and announced only after an agreement is reached which looks quite difficult as leaks will put a lot of pressure on the administration. Obama is also more focused internally and Iran’s regional hegemony is under attack because Syrian crises so the more likely scenario seems to be the continuatipon of the same non-working policies of the previous years.

“Regean reached with China”

It was not REGEAN that opened ties with China, it was NIXON.

No, they are not right technically because technically you need to have prices rise by 50% in ONE MONTH. And money supply must rise with inflation to keep fueling it. Nothing of the sort happened in Iran. High inflation and hyperinflation are two different things. There is no complete melt-down of the economy, except for people whose wealth (future wealth?) was in USD. Those people happen to think that they are the whole country.

Another wonderful post. I guess the hyperinflation folks have learned their lesson in economics by now. But with regard to a recent Ahmadinejad interview, I wanted to ask what if Iran had implemented the whole subsidy reform program in ONE GO before the sanctions, would it have been a wise decision? How would the inflation and economy be today if all other things assumed to be equal? Would Iran be in a better situation if all the subsidies had been scrapped just before sanctions?

Dear Dr. Hamid H.,

In the absence of a quick response from the professor, I shall take the liberty of squeezing an observation in between. You ask:

“what if Iran had implemented the whole subsidy reform program in ONE GO?”

Probably you mean energy subsidies, which the parliament has defined as the difference between local prices for different fuels and 90% of the average energy prices, FOB Persian Gulf. Since the first set of figuers is in Rials and the second figure is in Dollars, this introduced some complication into the calculation. The President was daring enough to undertake the first phase of the subsidy reform without listening to small voices that warned his economic team that USD/Rial parity (subsidised exchange rate) should first be adjusted, to account for eleven years of domestic inflation, making it possible to calculate the actual fuel subsidies.

Now that this has been allowed to happen and the parity is finding its market value, the extent of fuel subsidies has surprised them all.

The amount of energy in one littre of petrol, diesel fuel, fuel oil and one cubic meter of natural gas are within a bandwidth of 20%. But their domestic prices, after the accomplishment of the first stage of increase is still in the range of 700 to 7,000 Rials, a bandwidth of 1000%. And to remove subsidies in one go requires taking these prices to a level of IRR28,000 (USD 0.85 x 33,000 – 90% of average FOB Persian Gulf x estimated USD market parity). This is a price hike to the tune of 400% to 4,000% depending on the type of fuel. Unless all the cash thus generated is used to pay government debt, the fuel price increase will cause further inflationary pressure and require another adjustment in exchange rates and another correction to completely remove subsidies.

All in all I think this should be undertaken : Marg yekbaar, shivan yekbaar. Then, for the first time in forty years we can estimate the economic feasibility of public and private projects. As always I await guidance from Dr. Salehi, to whom I owe yet another appology.

Thanks for chiming in. You are rich subsidies have crept in to the tune of 50%, but not as much as you say. I would not use the free market exchange rate to determine the extend of the subsidy or any future price of energy in Iran. What if 1000 very rich people tried to take their money out of the country and $ went to 50000 rials, should everyone pay higher energy prices?

The best policy in my view is to have a formula for base energy prices linked to international markets and use taxation and non-linear prices to reach more equitable outcomes. I think high octane fuel, for example, should not carry a subsidy and should in fact pay a tax.

Dear Baddu,

Thank you for your elaborate response. I also think like you that marg yekbar, shivan yekbar.

Well, the subsidy program did go into effect about a year before the enhanced sanctions regime went into effect, and it eliminated subsidies for a while. The economy was not better off immediately. Such large scale economic surgery takes time before its benefits start coming in. Two things had to happen even in the absence of sanction for the benefits to accrue: first prices had to be allowed to rise so relative prices could adjust to new energy prices. Then, second, the rial had to depreciate to correct for past overvaluation. With those changes industries that took advantage of Iran’s workforce, rather than its cheap energy, would have attracted investment. Instead, Iran had a “dirty price control regime” which help some prices constant while others increased, causing a rather arbitrary adjustment in relative prices. And devaluation was delayed until sanctions hit and things started to come apart.

To answer your question about being better off if subsidies were removed, you can try to answer this question: Would Iran be better off now if energy prices were halved? Would Turkey be better off its energy prices were slashed?

It is difficult to answer that question, but theoretically lower energy cost should benefit the society. But I guess, the problem here is the estimation of real cost. Am I wrong? Do you think at the end the surgery will deliver its original goals now with sanctions essentially imposed forever?

Thank you.

Yes, subsidized energy benefits production (not the economy) but hurts the environment and is regressive. It is therefore terrible policy if your goal is to raise productivity.

Greetings Dr. Salehi-Isfahani,

My name is Enrique Maduro, and I’m working with Orlando Monagas on our Degree Research Paper on Iran’s Subsidy Reform’s impacts. We are form the Universidad Metropolitana in Venezuela, and we have read your work about the impact of the reform on households and almost every single one of your blog posts on the subject. They have been very helpful in sight that, as you mention, there is almost no official information about Iran’s economy in the recent years. The information we have gathered from your publications have been very valuable for our work, and is because of that that we would much appreciate if you accept us to interview you via email, skype, phone or facetime.

Thank you for your time.

Best Regards,

Enrique Maduro & Orlando Monagas

enriquemaduro91@gmail.com