Is Iran’s inflation moderating?

Note: A hiccup on the WordPress.com site caused this post to be removed after it was published on August 29. I am reposting it here with minor edits.

After some delay, the Statistical Center of Iran (SCI) has published its inflation report for the Iranian month of Mordad that ended on August 20. The report shows that prices were rising faster than in recent months, at 45.3% annual rate compared to an average of 27% for the preceding two months. The report undermines government hopes that inflation might come down to “around 30%” by the year’s end, a goal that the new Central Bank governor, Mohammad Reza Farzin, has been communicating to reporters. He has put inflation control as his main focus.

The Mordad inflation report did more than undermine this informal goal. The delay in publishing the report, even by a few days, prompted some critics to charge government suppression of bad economic news, and by implication admission of failure in controlling inflation. Instead of publishing it on the SCI website as in common practice, the report was given to a friendly news outlet several days before it appeared on the SCI site. I do not know the reasons behind the unusual dissemination route, but it did not help the management of inflation expectations, which is necessary if actual inflation is to come down, and for which data transparency is a must.

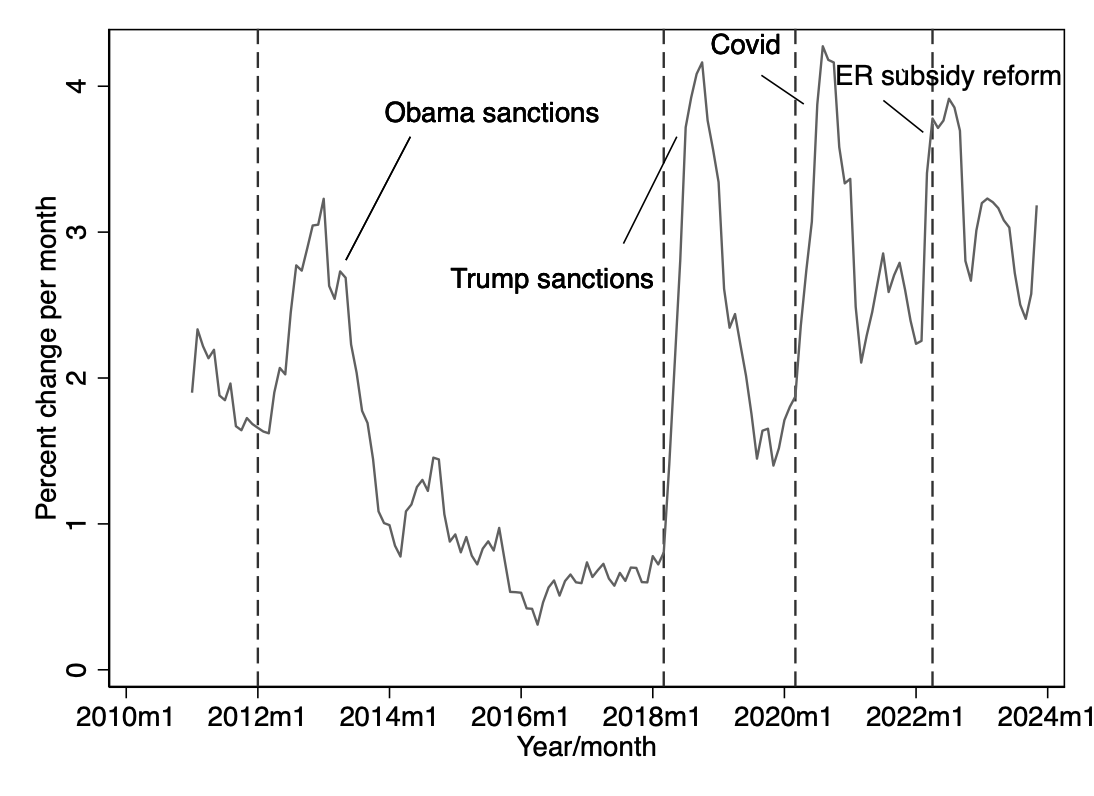

Bringing inflation expectations down is no easy task in Iran. Barely a year has passed since the country experienced its highest episode of inflation. In spring 2022, following the Russian invasion of Ukraine and the removal of food subsidies in Iran, prices shot up, reaching 300% annual rate in June (see the spike labeled exchange rate subsidy reform in Figure 1 for spring 2022).

It is difficult to know if the reasons for the high inflation of 2022 are behind us. The Ukraine war is still raging and food subsidies continue, albeit at a lower rate than before the subsidized exchange rate for essential goods was raised from 42,000 rials per USD to 285,000 rials–still well below the market rate of about 500,000 rials.

Having said that, I am less pessimistic than the World Bank about the future of prices. In its latest projections it forecast an inflation rate of 49.6% rate for 2023. Two new development suggest that, barring new external shocks, inflation could remain below 40% for the year. First, the events surrounding the rial’s newfound strength will probably continue for the rest of the year. The US dollar is about 10% cheaper, which in real terms means it is down by about 25% in the real terms. News of Iran’s higher oil sales, partial release of its frozen funds (some as part of the anticipated prisoner swap), and the invitation from BRICS this month to join the group, all contributed to the stability of the rial and through it to lower inflation.

Second, since January the Central Bank has followed a tighter monetary policy, mainly through credit restrictions. Credit restrictions have cooled off the real estate market and probably the market for foreign currencies. As always, the negative side of fighting inflation is reduced economic growth, even a recession. It is likely to cut the 4% GDP growth per year that Iran has experienced in the past two years. This may be why the latest forecast from the World Bank is about 2% for this year and beyond. Why prices would rise faster than last year while growth is halved, the WB report does not explain. But if the inflationary spiral can be broken and rate of price increases lowered to below 20%, halving the growth rate for a year or two may be worth it.

leave a comment